LLM statistics 2026: Adoption, market growth, and trust data

Jul 07, 2026

/

Daniela C.

/

10 min Read

Large language model (LLM) adoption has moved past the experimentation phase. Today, 88% of organizations use AI in at least one business function; ChatGPT’s market share has slipped below 50% for the first time as competitors gain ground, and worldwide AI spending is on track to reach $2.59 trillion.

The real question now is whether trust and governance are keeping pace with that growth, and the data suggests they aren’t.

Inaccuracy has overtaken every other concern as the top-cited AI risk, jumping 14 percentage points in a single year, while confidence in how well organizations respond to AI incidents is falling even as usage climbs.

Top LLM statistics you should know in 2026

From enterprise surveys to market forecasts, the data shows LLMs have become core business infrastructure, even as trust in their output hasn’t caught up with how widely they’re used.

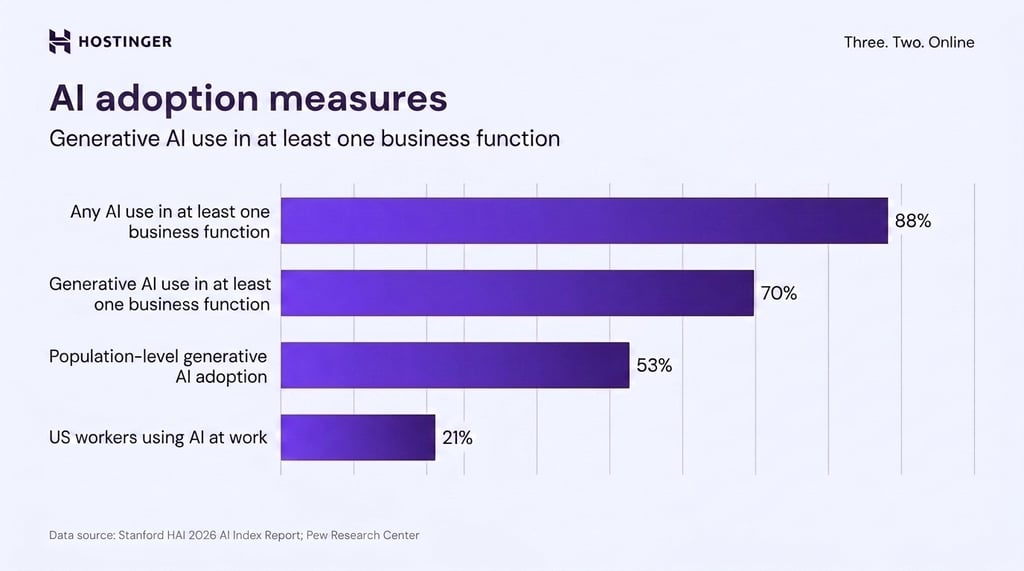

- 88% of organizations worldwide now use AI in at least one business function.

- 70% of organizations use generative AI specifically in at least one business function, though agentic AI deployment remains in the single digits across almost every function today.

- Worldwide AI spending is on track to reach $2.59 trillion in 2026, a 47% jump from 2025.

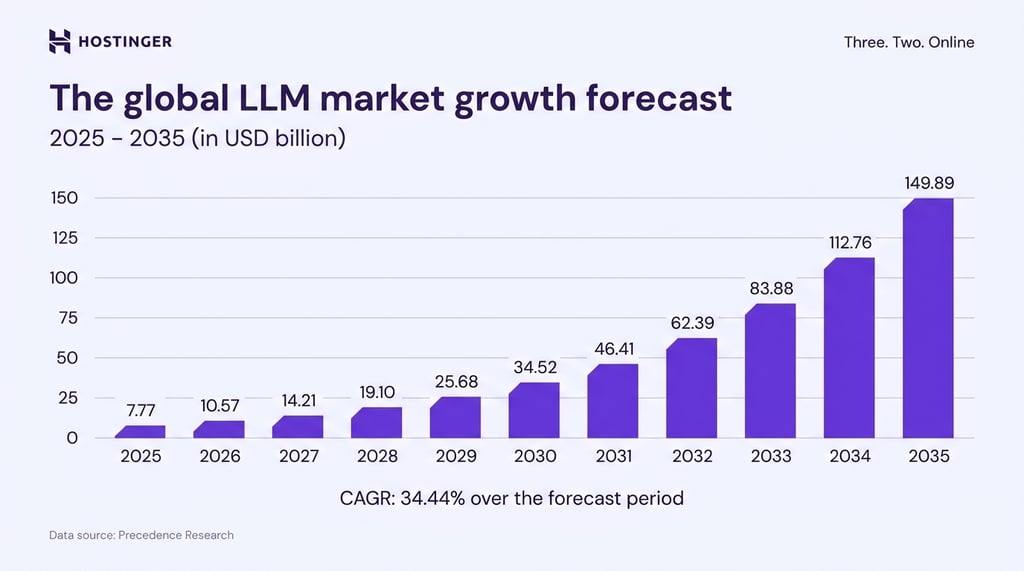

- The global LLM market is projected to reach nearly $150 billion by 2035, up from $10.57 billion in 2026.

- ChatGPT’s market share has fallen below 50% for the first time, though it still leads with over 1.1 billion monthly users.

- Anthropic now commands 40% of enterprise LLM API spend, while OpenAI’s enterprise share has fallen from 50% to 27% over the same period.

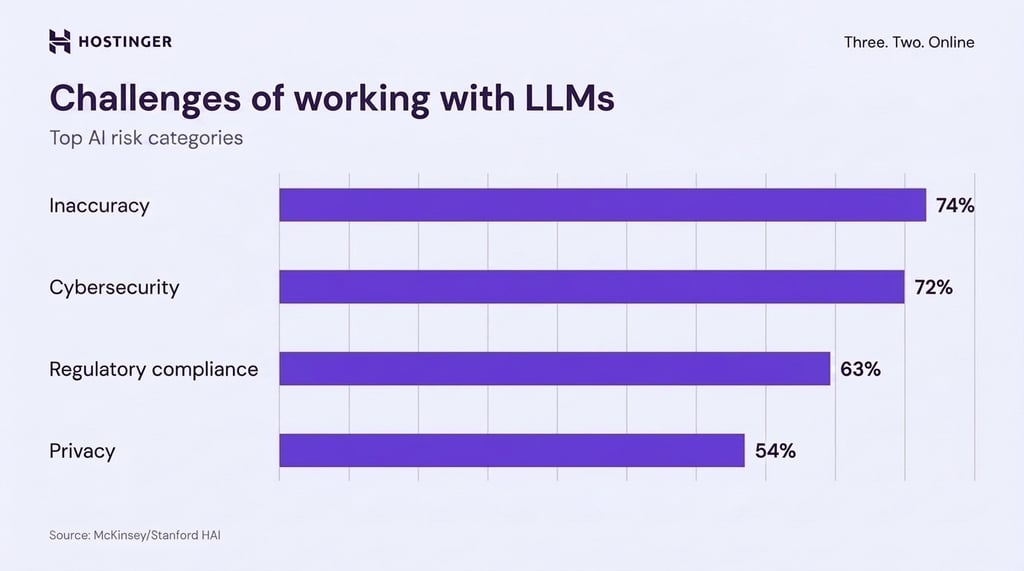

- 74% of organizations now cite inaccuracy as their top AI risk, up 14 percentage points in a single year, ahead of cybersecurity (72%).

- Nearly 3 in 4 companies (74%) plan to deploy agentic AI within two years, up from 23% using it moderately today, yet only 21% report having a mature governance model for autonomous agents.

- Hallucination rates across 26 leading foundation models range from 22% to 94%, meaning even top-performing models are wrong roughly one in five times.

- 77% of companies now factor an AI solution’s country of origin into vendor selection, and 58% build their AI stack primarily with local vendors, as sovereign AI becomes a boardroom issue.

How widely have businesses adopted LLMs?

LLM adoption inside organizations has gone from a minority practice to the default in under three years, though depth still lags breadth. Hostinger’s own AI statistics survey of 1,000 US business leaders found only 20% had implemented AI across multiple functions or fully integrated it into their operations, even though far more report using it somewhere.

- 88% of organizations use AI in at least one business function, up from 78% the year before and roughly 20 points ahead of the 67% (Stanford HAI).

- 70% of organizations use generative AI specifically in at least one business function, up sharply from 33% just two years earlier. Agentic AI deployment, by contrast, remains in the single digits across nearly every function measured (Stanford HAI).

- Generative AI reached 53% population-level adoption within three years, a faster curve than the PC or the internet, though adoption correlates strongly with GDP per capita and varies widely by country, from 61% in Singapore to 28.3% in the US, which ranks 24th globally despite leading in AI investment (Stanford HAI).

- 21% of US workers say at least some of their work is done with AI, up from 16% the year before. Workers with a bachelor’s degree or higher account for most of that increase, rising from 20% to 28% (Pew Research Center).

- 58% of employees globally report using AI on a semi-regular or regular basis, with usage exceeding 80% in India, China, Nigeria, the UAE, and Saudi Arabia, compared with 40–48% across most of North America and Europe (Stanford HAI).

Adoption is no longer the question. The organizations pulling ahead now are the ones moving past pilots into scaled, governed deployment, which Stanford HAI’s data suggests is still a much smaller group than the 88% headline implies.

LLM market size and growth

Market size estimates for LLMs vary between research firms, largely because they define “the LLM market” differently. Some scope it to foundation models and APIs; others include the full software and services stack built on top of them. Treat the figures below as directional rather than precise, and prefer one consistent source when citing them together.

- The global LLM market is set to grow about 36% in 2026 alone, from $7.77 billion to $10.57 billion, then keep compounding at roughly 34% a year to reach close to $150 billion by 2035 (Precedence Research).

- North America holds the largest regional share at 33%, with the US market on track to grow nearly 20-fold, from $1.92 billion to $37.98 billion by 2035. Asia-Pacific is expected to be the fastest-growing region over the same period (Precedence Research).

- By segment, chatbots and virtual assistants lead applications at 28% share, and on-premises deployment leads at 59%, the latter driven by data privacy requirements in regulated industries, though cloud deployment is expected to grow faster from here (Precedence Research).

- By industry vertical, healthcare now leads the market, a shift from retail and ecommerce’s earlier 27.5% lead (Market.us), with finance projected to grow fastest (Precedence Research).

- Worldwide AI spending, a broader category than the LLM market specifically, is set to grow 47% in 2026 to reach $2.59 trillion (Gartner).

- Enterprise-specific generative AI spending tripled year-over-year, from $11.5 billion to $37 billion, with AI applications now representing about 6% of the entire software market (Menlo Ventures).

The spread between market forecasts, from roughly $10 billion up to $2.59 trillion depending on scope and firm, is a reminder that “the LLM market” and “AI spending” aren’t interchangeable terms, even though they get used that way in casual reporting.

Which LLMs lead the market?

There’s no single answer to how many LLMs exist. Hugging Face hosts hundreds of thousands of model repositories, but most are fine-tunes or experiments rather than distinct models.

Narrowing to actively maintained, ready-to-run LLMs still gets you a large and fast-growing number: Ollama’s library alone lists hundreds of actively maintained models across dozens of families, with one tracker counting over 4,500 curated and community entries as of June 2026, up sharply from a couple hundred just two years earlier.

That’s before counting proprietary models that never get published openly at all. Model count keeps climbing, but LLM market share tells a very different story: it’s concentrated, and it’s shifting fast.

The consumer AI chatbot market looked like a one-player story as recently as mid-2025. That’s no longer true, and the enterprise market has moved the same way, but faster.

- ChatGPT’s consumer market share dropped below 50% for the first time in 2026, as users increasingly switch between assistants (TechCrunch).

- ChatGPT still leads by a wide margin with over 1.1 billion monthly users, becoming the fastest app ever to reach that milestone (Reuters).

- Google’s Gemini has grown to 662 million monthly users, largely on the strength of its integration across Google’s existing products, while Anthropic’s Claude has reached 245 million, with a strong reputation specifically in productivity and coding use cases (TechCrunch).

- The top three AI assistants now account for 89% of time spent on AI assistant apps, meaning the remaining field, including AI companion and content-generation apps, stays fragmented and open to new entrants (TechCrunch).

- In the enterprise specifically, Anthropic now commands 40% of LLM API spend, up from just 12% in 2023, driven largely by dominance in coding tools. OpenAI’s enterprise share has fallen from 50% in 2023 to 27% in the most recent count, while Google has grown from 7% to 21% (Menlo Ventures).

For businesses choosing an LLM provider today, that volatility is the real takeaway. The safer bet isn’t picking today’s leader; it’s building on tooling flexible enough to switch providers when the market moves again.

Expert tip

The LLM market is maturing the same way cloud did a decade ago. Early adopters picked whoever was most impressive, and then the enterprise wave came in and picked whoever was most dependable. We’re in that second wave now, and it’s reshaping the competitive landscape faster than most people expected.

LLM usage statistics

LLMs are becoming a normal part of daily work, but not evenly across all domains. Usage and sentiment still split sharply along gender lines, even as the tools themselves get more capable and more widely available.

- A clear gender gap in AI usage and sentiment persists into 2026: 69% of men say AI is a “valuable assistant and collaborator” versus 61% of women, and women are meaningfully more likely to say using AI at work “feels like cheating” (SurveyMonkey).

- General-purpose chatbots like ChatGPT and Gemini remain the most common entry point: 27% of US workers use them daily or weekly, among the 40% who’ve used any AI tool at work in the past year (SurveyMonkey).

- 87.9% of professionals rate AI’s impact on their work quality as 6 or higher out of 10, with 26.3% giving it a perfect score, while 9% report declining quality after using AI (Amperly).

- 51.7% use LLMs for research and information gathering, 47% for creative writing, and 45% for email and communications, with coding and scripting use (27.3%) notably higher than the share of respondents whose job actually involves coding (Amperly).

- 84% of developers worldwide now use or plan to use AI coding tools, up from 76% in 2024 (Hostinger’s vibe coding statistics).

The productivity gains are real, but confidence in them hasn’t kept pace. That gap between what people report experiencing and how much organizations actually trust the technology is exactly where the data below picks up.

LLM trust, risk, and security concerns

As LLMs move from answering questions to taking autonomous actions through AI agents, trust and governance have become the harder problem.

Where trust stands today

- Average responsible-AI maturity rose to 2.3 in 2026, up from 2.0 the year before, on a 4-point scale that scores how far organizations have progressed across AI strategy, risk management, and governance (McKinsey).

- Only about 30% of organizations have reached maturity level 3 or higher in strategy, governance, and agentic AI controls specifically, even as overall maturity improves (McKinsey).

- The share of organizations with no responsible-AI policies at all dropped from 24% to 11% year-over-year, while AI-specific governance roles grew 17% in 2025, indicating governance is professionalizing even if it hasn’t caught up with usage (Stanford HAI).

- Organizations investing $25 million or more in responsible AI report meaningfully higher maturity scores and are far more likely to see AI’s impact exceed 5% of EBIT, suggesting trust investment pays for itself rather than slowing innovation down (McKinsey).

Emerging risks

- 74% of organizations now cite inaccuracy as their top AI risk, up 14 percentage points in a single year, overtaking every other concern including cybersecurity (72%), regulatory compliance (63%), and privacy (54%). This figure is corroborated almost exactly across both McKinsey’s and Stanford HAI’s independent surveys (McKinsey; Stanford HAI).

- Hallucination rates across 26 leading foundation models range from 22% to 94%, meaning even the best-performing models produce inaccurate output roughly one in five times, per Stanford’s own benchmark testing (Stanford HAI).

- Nearly two-thirds of organizations cite security and risk concerns as the top barrier to scaling agentic AI, ahead of regulatory uncertainty or technical limitations (McKinsey).

- Active risk mitigation lags behind risk awareness in nearly every category, most notably for intellectual property infringement and personal privacy, where organizations recognize the risk faster than they build controls for it (McKinsey).

- AI incident rates have held steady at around 8%, but almost 60% of organizations that experienced an incident rate their own response as only satisfactory or worse, pointing to a widening gap between system complexity and organizational readiness (McKinsey).

How organizations are responding

- Nearly 60% of organizations cite knowledge and training gaps as their leading barrier to responsible AI implementation, up from about 50% the year before (McKinsey).

- Organizations with clear, assigned ownership for responsible AI score 2.6 on average versus 1.8 for those without it, making explicit accountability one of the strongest predictors of maturity (McKinsey).

- 90% of companies expanded their privacy programs in direct response to AI, and 93% plan further investment, reflecting how quickly AI has pushed data governance up the list of executive priorities (Cisco).

- Outright bans on generative AI use fell 21 percentage points year-over-year, as organizations shift from blocking AI outright toward enabling it with governance (Cisco).

- Concern about generative AI’s risk to intellectual property and copyright fell from 69% to 55% year-over-year, even as concern about inaccuracy rose elsewhere, suggesting organizations’ risk priorities are shifting rather than uniformly increasing (Cisco).

That gap between concern and control becomes even sharper once AI stops just answering questions and starts taking action on its own.

Agentic AI: adoption is outpacing governance

The clearest evidence of the trust gap lies in how organizations are handling AI agents, specifically, systems that don’t just answer questions but take actions on their own. Deloitte’s State of AI in the Enterprise report quantifies the gap directly, tracking how enterprises are moving (or not moving) from AI pilots to full agentic deployment.

- 23% of companies use agentic AI at least moderately today, but 74% expect to within two years, with 5% expecting agents to be fully integrated as a core part of operations (Deloitte’s State of AI in the Enterprise).

- Only 21% of companies report having a mature governance model for autonomous agents, despite the sharp adoption curve ahead, which is the same access-versus-governance gap McKinsey and Stanford HAI document above, just measured a different way (Deloitte’s State of AI in the Enterprise).

- Data privacy and security is the top AI-related concern for 73% of organizations, ahead of legal and regulatory compliance (50%) and governance capabilities and oversight (46%), closely mirroring the inaccuracy-and-cybersecurity concerns McKinsey and Stanford HAI report (Deloitte’s State of AI in the Enterprise).

- 85% of companies expect to customize agents to fit their specific business needs rather than deploy off-the-shelf agent products, reflecting how early and unsettled the tooling landscape remains (Deloitte’s State of AI in the Enterprise). This is part of why AI agent products built for a specific job, like handling routine business tasks or connecting an AI assistant directly to infrastructure it can act on, are gaining traction faster than general-purpose agents: tools such as Hostinger’s AI Agents are built around that same idea of narrow, task-specific autonomy rather than open-ended agent behavior.

- Sovereign AI has become a genuine boardroom issue; 77% of companies now factor an AI solution’s country of origin into vendor selection decisions, and 58% build their AI stack primarily with local vendors, up sharply as organizations weigh data residency and compute location alongside model capability (Deloitte’s State of AI in the Enterprise).

- The same security gap shows up in dedicated agent-risk research: 82% of organizations already use AI agents, but only 44% have security policies in place to govern them, and 80% report their agents have already taken unintended actions such as accessing unauthorized systems or sharing sensitive data (SailPoint).

- The global agentic AI market is projected to grow from $9.14 billion in 2026 to $139.19 billion by 2034, a 40.5% compound annual growth rate (Hostinger’s agentic AI statistics).

The agentic AI numbers matter for LLM statistics specifically because agents are built on top of LLMs. As more of them get permission to act (sending emails, modifying records, deploying code) rather than just draft or summarize, the same governance gap documented above stops being an abstract risk-survey answer and starts being an operational one.

Developer-facing tools already show this shift in practice: an MCP-based connector that lets an AI coding assistant deploy sites or manage server settings directly from an IDE, the kind of capability Hostinger Connector provides, is exactly the sort of ‘agent takes action’ use case driving that governance gap in the first place.

Expert tip

Adoption was never really the hard part. Getting an LLM into a workflow takes a weekend. Getting an organization to trust what it produces and to build the review and governance habits around that takes years. The gap between those two timelines is exactly where most of today’s AI incidents come from.

The future of LLMs

Enterprises are moving from “should we use AI” to “how much of our operations should it run,” and the forecasts below reflect that shift.

- By 2026, 30% of enterprises are expected to automate more than half of their network operations using AI, up from under 10% in mid-2023. Since this is the target year for that prediction, it’s worth checking for a Gartner follow-up confirming actual outcomes (Gartner).

- Agentic AI usage is expected to jump from 23% today to 74% within two years, a faster ramp than physical AI (robotics, automated machinery), which is projected to grow from 58% to 80% over the same window (Deloitte).

- AI-related job postings requiring agentic AI skills surged over the past year, alongside a nearly 20% decline in employment for software developers aged 22–25 from their 2024 peak, suggesting the disruption is landing unevenly by career stage rather than across the workforce broadly (Stanford HAI).

- Globally, 59% of people now say AI products have more benefits than drawbacks, up from 55% the year before, even as 52% separately report feeling nervous about AI-powered products, a combination that mirrors the trust-versus-adoption gap seen throughout this article (Stanford HAI).

The organizations that benefit most from LLMs in the next few years aren’t necessarily the ones deploying the most models. Based on the trust and risk data above, they’re more likely to be the ones closing the gap between adoption and governance early, since that gap is where most of the current risk and most of the current opportunity sit.

All of the tutorial content on this website is subject to Hostinger's rigorous editorial standards and values.

Daniela is an Off-Site SEO Specialist with extensive expertise in link building, digital PR, and content optimization. She has led international outreach campaigns across the U.S., Brazil, France, and Spain, securing high-quality backlinks. Follow her on LinkedIn.