How to become an entrepreneur and launch your business

Mar 12, 2026

/

Alma

/

14 min Read

Becoming an entrepreneur starts with identifying a problem and building a solution people are willing to pay for. Many successful businesses begin this way – by testing an idea, building a simple product, and improving it based on customer feedback.

Here are the eight steps on how to become an entrepreneur and launch a business:

- Find a real problem to solve

- Validate your idea

- Build the first version of your product

- Create a scalable business model

- Develop an entrepreneurial mindset

- Build and connect with your professional network

- Fund your venture

- Register your business and go live

You don’t need a groundbreaking invention or large startup capital to start. What matters most is testing ideas early, learning from real customer feedback, and improving your business as you grow.

1. Identify a real problem to solve

Successful entrepreneurs start by identifying a real problem that people are willing to pay to fix. In India, many successful businesses begin this way by noticing everyday frustrations in areas like local services, education, or online shopping, and building a solution around them.

Look at situations where people struggle to find reliable services, affordable products, or convenient ways to buy. For example, a neighborhood might lack a dependable home cleaning service, a small restaurant may need an easier way to take online orders, or students might struggle to find affordable tutoring. Each of these gaps can become a business opportunity if enough people share the same problem.

It’s tempting to build a business around something you personally enjoy. However, focusing on real customer needs is far more important. Passion can keep you motivated, but paying customers are what make a business sustainable.

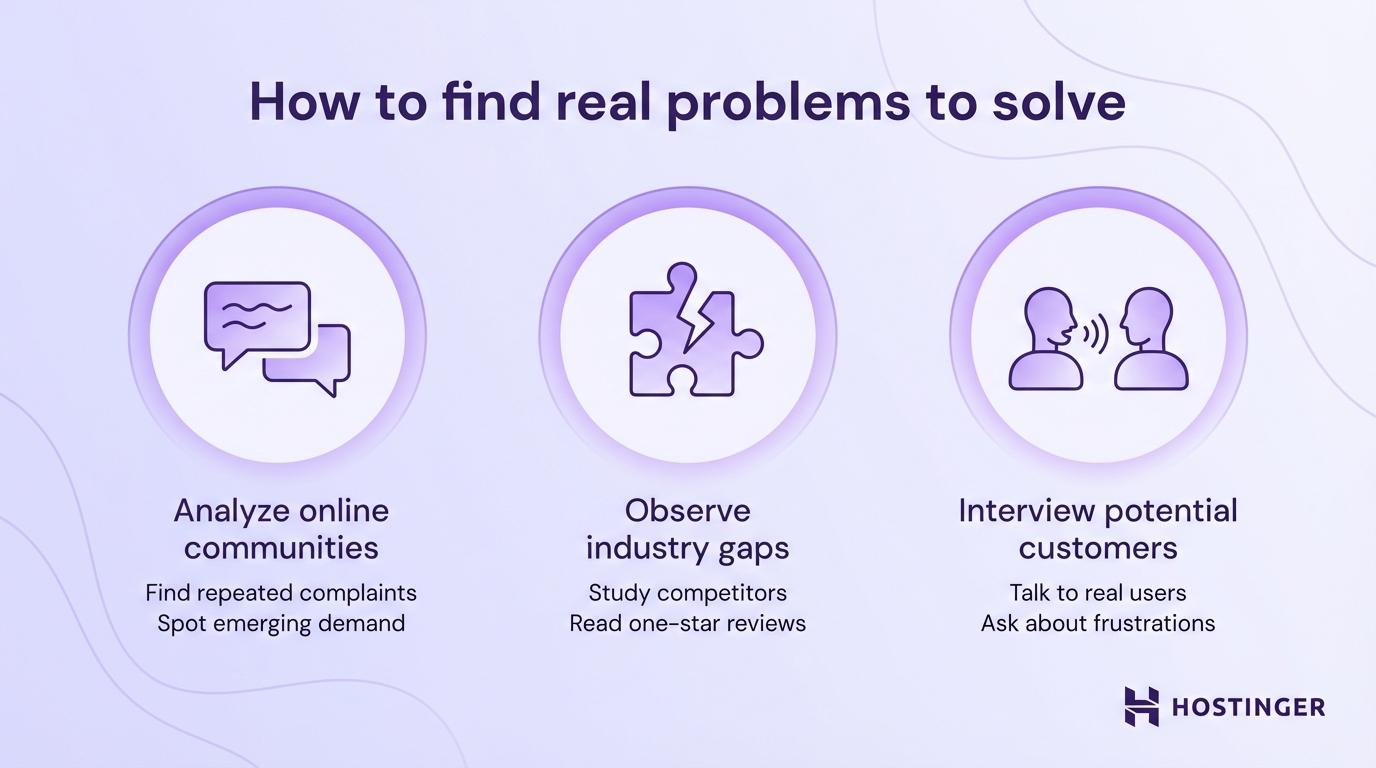

Here are three ways to find problems that your business can potentially solve:

- Analyze online communities. B In India, many discussions also happen on WhatsApp groups and Instagram pages. Look for recurring complaints, questions, or posts where people say things like “I wish there was a service that…”. Watching business trends also shows where demand is heading before the market catches up.

- Observe industry gaps. Study companies in industries that interest you. Read negative reviews on Google Maps, Amazon, or Flipkart to understand what customers dislike. These reviews often highlight service gaps that new entrepreneurs can improve.

- Interview potential customers. Speak with 10–15 people who fit your target audience, such as students, freelancers, or small business owners. Ask about their biggest frustrations or daily challenges. Instead of asking if they would buy your idea, focus on understanding the problems they face.

Many successful small Indian businesses started this way: someone noticed a common frustration, confirmed that others experienced it too, and built a solution around it.

Once you clearly understand the problem and confirm that people experience it regularly, the next step is validating whether they are willing to pay for your solution.

2. Validate your business idea

Validating your business idea means confirming that real people will spend money on your solution before you invest months building it. Skipping this step is one of the main reasons new businesses fail, because they build something nobody asked for or can’t find the right fit between their product and the market.

So how do you avoid that? Use the lean startup methodology. It flips the traditional business model on its head. Instead of spending months writing a business plan, building a full product, and then hoping customers show up, you start by talking to customers first. You test small. You learn fast. And you only build what people actually want.

Think of it this way: instead of betting everything on one big launch, you run a series of cheap experiments. Each one tells you something. Did people click? Did they sign up? Did they pay? If yes, keep going. If no, adjust. The whole point is to fail quickly on the small stuff so you don’t fail slowly on the big stuff.

Here’s a four-step process to put this into practice:

- Talk to 10–20 target customers. Go beyond casual conversations. Ask specific questions about how they currently deal with the problem, what they’ve tried, and how much they’ve spent on failed solutions. If people aren’t actively trying to fix the problem, they probably won’t pay you to fix it either.

- Create a simple landing page. Build a single webpage that describes your product or service, explains the benefit, and includes a signup form or waitlist. You don’t need the actual product yet – you need to see if the promise alone attracts interest.

- Pre-sell the product or service. Offer early access at a discount in exchange for payment upfront. This is the strongest form of testing because it involves real money. If 5 out of 20 people pay before the product even exists, you’re onto something.

- Measure interest. Track how many visitors sign up, how many complete a purchase, and where people drop off. These numbers tell you whether the market demand is strong enough to justify building the full version.

Recent small business statistics show that 28% of entrepreneurs spend between ₹41,00,000 and ₹1,43,00,000 ($50,000–$175,000) just to get started, and about 18% of new businesses close within their first year. Testing your idea early helps you avoid investing large amounts of money into a product or service that the market doesn’t actually want.

The goal of validation is simple: learn quickly and avoid building something nobody wants. Once you confirm that customers are interested and willing to pay, you can proceed to create the first version of your product or service.

3. Build a minimum viable product

A minimum viable product (MVP) is the simplest version of your idea that still solves the core problem. It’s not a rough draft of everything you want to build – it’s a focused test of your most important assumption.

The goal of an MVP isn’t to impress anyone. It’s to learn. You’re putting something real into people’s hands so you can watch how they use it, where they get stuck, and what they actually care about versus what you thought they’d care about.

This is how you build and improve your MVP:

- Pick the core feature. Ask yourself: what’s the one thing this product must do to be useful? Everything else is a distraction right now.

- Cut everything extra. If a feature doesn’t directly serve the core problem, remove it. You’ll add it later if feedback confirms it matters.

- Launch quickly. Speed beats polish at this stage. A working product that’s live in three weeks teaches you more than a perfect product that takes six months.

- Collect feedback. Ask early users what’s working, what’s confusing, and what they wish it could do. Pay attention to what they do, not just what they say.

- Improve and repeat. Use that feedback to make changes, add what’s missing, or remove what’s not working. Then test again.

Say you want to create a digital product, like a meal-planning app. Your MVP isn’t a full app with 500 recipes, a shopping list, and AI recommendations. It’s a simple spreadsheet-based plan you email to 20 subscribers each week. If they open it, use it, and ask for more – you’ve proven the concept without writing a single line of code.

Testing early versions this way keeps your costs low while you’re still learning. Each round of feedback gets you closer to a product the market genuinely wants.

The MVP approach works especially well for product-based businesses. Even starting an ecommerce business without money is possible when you keep your first version simple and test before you invest.

4. Develop a scalable business model

Your business model is how you make money – who pays you, what they pay for, and how much it costs you to deliver. Getting this right determines whether your tested idea becomes a real business or an expensive hobby.

There are five questions you need to answer to create a business model that works for you:

- What makes you different? What specific problem do you solve, and why is your solution better than the alternatives? Your value proposition should be one clear sentence, not a paragraph.

- Who are you selling to? “Everyone” isn’t an answer. Narrow your target market by age, behavior, location, or the specific pain point they share.

- How do you charge? Options include one-time purchases, subscriptions, freemium tiers, commissions, or licensing. Each model has different cash flow effects. Subscriptions give you a steady monthly income. One-time sales require you to constantly find new buyers.

- What does it cost you? List every expense involved in delivering your product or service – tools, hosting, labor, marketing, transaction fees. Your revenue needs to clear these costs by a healthy margin, or the math doesn’t work.

- How do customers find you? Your own website, marketplaces, social media, referrals, or partnerships all work differently depending on your audience. In India, many new businesses start by attracting customers through Instagram, WhatsApp Business, or marketplaces like Amazon and Flipkart before expanding to their own website.

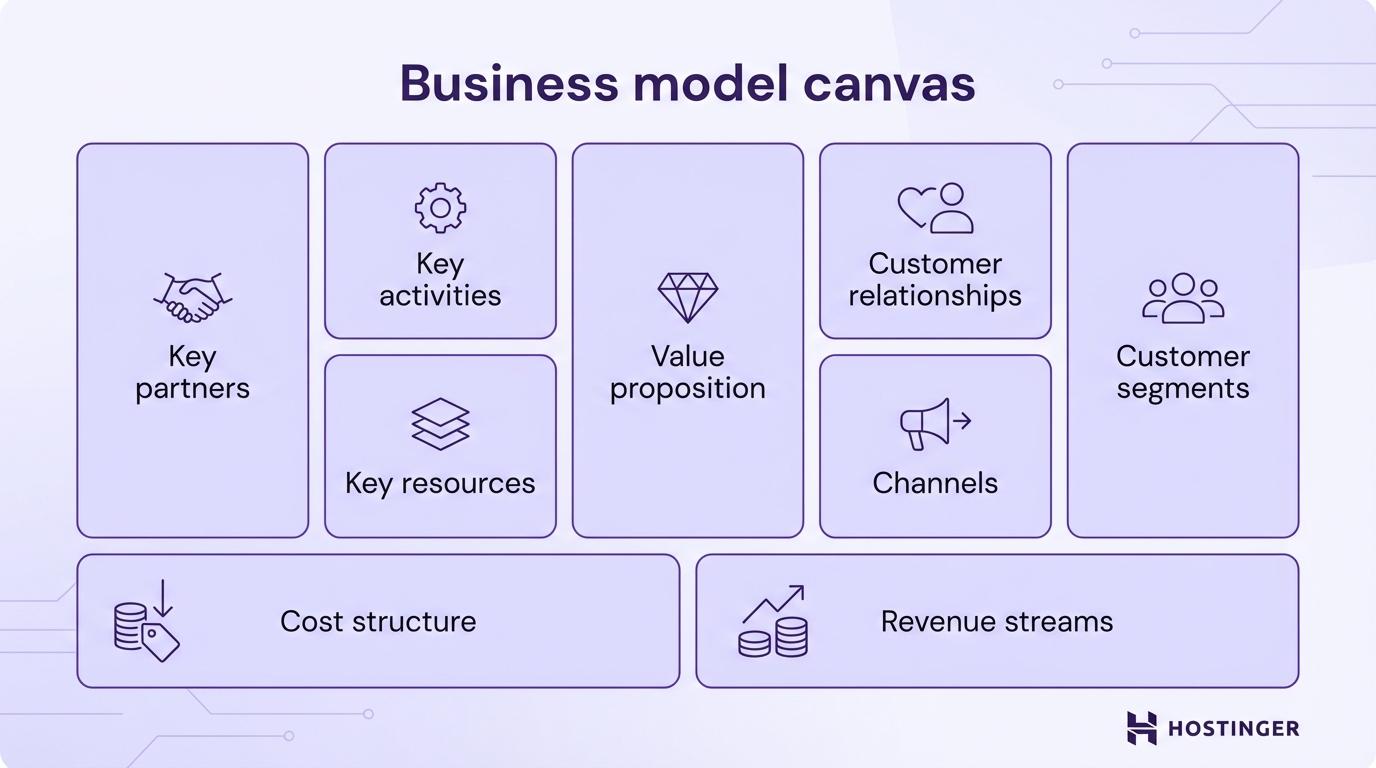

The Business Model Canvas, originally developed by Alexander Osterwalder, is a one-page, nine-block framework that puts all five of these pieces side by side. Instead of writing separate plans for your pricing, your audience, your costs, and your channels, you sketch them all on a single page. That’s where the value is. You start to see the connections.

For example, you might realize your target audience hangs out on Instagram, but your revenue model depends on long-form content that works better through email. Or that your cost structure only works if you hit a certain number of monthly subscribers, which changes how aggressively you need to market. These kinds of gaps are easy to miss when you plan each piece in isolation. On a canvas, they’re obvious.

You don’t need fancy software for this. A whiteboard, a spreadsheet, or even a sheet of paper with nine boxes works fine. The point is seeing your whole business at a glance so you can spot what doesn’t fit before it costs you money.

One of the first things that the canvas will pressure-test is your pricing — because it sits right at the intersection of your costs, your audience, and your revenue model.

Getting your pricing right is one of the trickiest parts. Charge too little, and you can’t cover costs. Charge too much, and you scare off early customers. Pricing a product well means finding the point where customers feel they’re getting real value and you’re still making healthy margins.

Your revenue model also depends on what you’re selling. Physical goods, digital products, and services each come with different cost structures and margins. The type of ecommerce you choose – whether B2C, B2B, or direct-to-consumer – shapes everything from how you price to how you deliver.

5. Cultivate an entrepreneurial mindset

An entrepreneurial mindset is the ability to treat setbacks as information and keep moving forward anyway. It’s not a personality trait you’re born with – it’s a set of habits you build over time.

Three qualities separate entrepreneurs who last from those who quit early: resilience, adaptability, and risk tolerance.

Resilience means bouncing back after a failed launch or a lost client without spiraling into self-doubt. Adaptability means changing direction when the numbers tell you to, even if you’re emotionally attached to your original plan. Risk tolerance means being comfortable making decisions without perfect information.

Entrepreneurship is experimentation. Your first idea probably won’t be your best one. Your first business model will almost certainly change. The people who succeed treat every failure as a rough draft, not a final answer.

Build these three habits into your weekly routine:

- Set aside time for learning. Spend two to three hours per week picking up something directly useful to your business – copywriting, sales, basic money management, or your industry’s tools. One new skill per month adds up fast.

- Get comfortable with your numbers. Learn to read a profit-and-loss statement, understand cash flow, and track how much you spend to earn each dollar. Most businesses don’t fail because of bad ideas – they fail because the founder ran out of money without seeing it coming.

- Practice networking. Reach out to one new person in your industry each week. Not to pitch them, but to learn from them. The relationships you build now become referrals, partnerships, and channels for advice later.

A growth mindset isn’t about blind optimism. It’s about building proof, one small win at a time, that you’re capable of figuring this out.

Many entrepreneurs build their confidence and income by testing the waters with popular side hustles before going all-in. That approach lowers risk while still giving you real-world business experience.

The same applies to making money online through freelancing, digital products, or content creation. In India, many founders begin by offering services such as freelance design, tutoring, consulting, or running a small online store before turning those projects into full-time businesses. These paths help build entrepreneurial skills while still generating income.

6. Build a professional network

Your network directly affects how fast your business grows. The right connection can introduce you to your first customer, a potential co-founder, or an investor – often faster than any marketing campaign.

Business networking isn’t about collecting business cards at events. It’s about building genuine relationships with people who understand your industry, your challenges, and your goals.

Here’s how to build your professional network:

- Attend industry events. Conferences, meetups, and workshops put you in the same room as people who share your interests and can offer perspectives you don’t have. In India, many entrepreneurs connect through startup events, local business meetups, and tech conferences in cities like Bengaluru, Delhi, or Mumbai. Even virtual events create meaningful industry connections if you follow up afterward.

- Join entrepreneur communities. Online groups like Indie Hackers, startup communities on LinkedIn, or local founder groups give you ongoing access to people building businesses at the same stage as you. Many Indian entrepreneurs also participate in startup incubator communities or regional founder groups. Make sure you show up regularly and contribute to discussions rather than visiting only once.

- Connect with mentors. Find someone two to three steps ahead of you and ask specific questions. Good mentorship doesn’t require a formal arrangement – it often starts with a single, thoughtful email asking for advice on a specific problem.

- Approach potential partners. Look for businesses that serve the same audience but don’t compete with you directly. Business partnerships with complementary companies let you share audiences, co-create offers, and split marketing costs.

Social proof builds faster in communities than in isolation. When other entrepreneurs vouch for your work, potential customers and investors notice. Your reputation in these circles becomes a credibility asset you can’t buy with advertising.

7. Secure funding for your venture

Most businesses need startup funding to cover early costs such as product development, marketing, and operations before revenue kicks in. The right option depends on how much you need, how fast you need it, and how much control you’re willing to give up.

This is how the main options compare:

| Funding option | How it works | Best for | Trade-off |

| Personal savings | You invest your own money upfront | Low-cost startups like service businesses, freelancing, or digital products | Full control, but limited to what you’ve saved |

| Bootstrapping | You reinvest business revenue instead of taking outside money | Businesses that can generate revenue early | Slower growth, but you keep full ownership |

| Small business loans | Banks, NBFCs, or government-backed schemes provide loans with structured repayment terms | You invest your own money up front | Requires a business plan, credit history, and sometimes collateral |

| Angel investors | Individual investors typically invest ₹20,00,000 to ₹4,00,00,000+ for a small stake in your company | Early-stage startups with traction and growth potential | You gain capital and mentorship, but give up partial ownership |

| Venture capital | Investment firms provide large funding rounds in exchange for equity | High-growth startups targeting large markets such as SaaS, fintech, or ecommerce | Fastest path to scaling, but you give up significant ownership and control |

Start with the cheapest money first – your own savings and revenue, and move toward outside capital only after you’ve proven the business model works. Each step up the table brings more cash but also more strings attached.

If you go after angel investors or venture capital, you’ll need a pitch deck. A strong pitch deck covers your problem, solution, market size, early results, team, and financial projections in 10–15 slides. Keep it clear, specific, and backed by real numbers from your testing.

8. Register and launch your business

Business registration becomes important once you start earning revenue, signing contracts, or taking on legal obligations. In India, some registrations are optional at the early stage, but formalizing your business helps you open a business bank account, access government programs, and work with larger clients.

Here’s the step-by-step sequence on registering your business:

- Choose your legal structure. The most common options in India are sole proprietorship, partnership firm, Limited Liability Partnership (LLP), and private limited company. A sole proprietorship is the simplest form of business ownership and is often used by freelancers and small local businesses. An LLP or private limited company separates your personal assets from business liabilities, which can protect your savings if something goes wrong. Many first-time entrepreneurs start with a sole proprietorship or LLP because they are relatively simple to set up.

- Register your business name. If you plan to operate under a brand name rather than your personal name, you may need to register the business, depending on the structure you choose. For example, company names are registered through the Ministry of Corporate Affairs (MCA) when setting up an LLP or private limited company.

- Get licenses and permits. Depending on your business type, you may need additional registrations such as GST registration, Shop and Establishment registration, or local municipal licenses. Online sellers may also need GST registration when selling through marketplaces like Amazon or Flipkart.

- Set up your accounting. Open a separate business bank account and use accounting software to track revenue and expenses. Monitoring your cash flow from the beginning helps you understand how money moves through your business and makes tax filing much easier.

- Launch publicly. Announce your business launch through your website, email list, and social channels. The first launch doesn’t need to be perfect. It needs to be public so real customers can find you and start giving you feedback. If building a website feels like a big time commitment, it doesn’t have to be. Tools like Hostinger Website Builder let you put together a professional-looking site in minutes.

Important! Talk to a legal or tax professional before choosing a legal structure, as the details vary by country and state.

Your business launch marks the shift from planning to doing. Everything before this point was preparation. Everything after is improvement, refining your product, growing your audience, and adjusting your strategy based on feedback.

What are the benefits of becoming an entrepreneur?

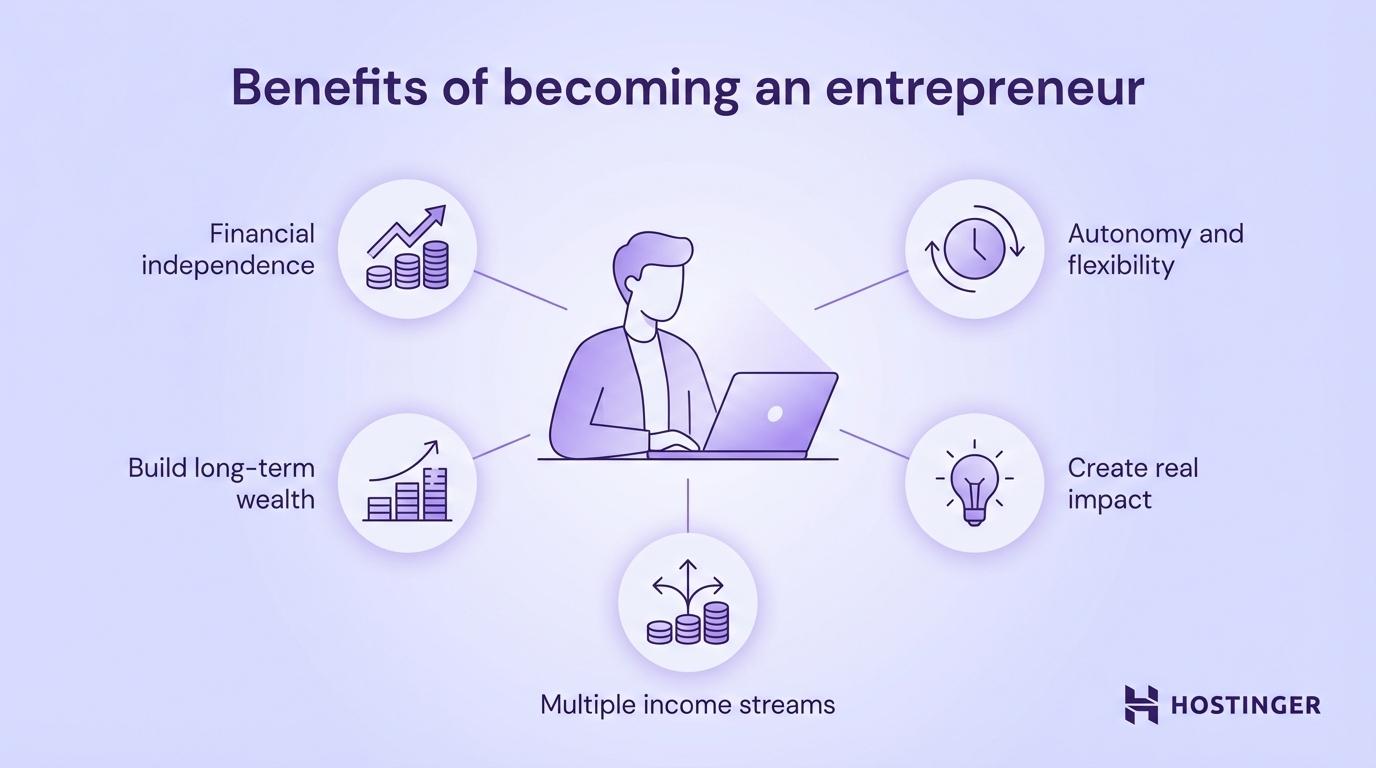

Financial independence is the most common reason people start businesses. As an employee, your income is capped by your salary. As a business owner, your earning potential is less limited by a fixed paycheck and more tied to the value you create and the decisions you make.

That financial upside comes with another benefit: autonomy and flexibility. You design your work around your life, not the other way around. You choose your hours, your projects, and who you work with. This doesn’t mean working less; most entrepreneurs work more in the early stages – but you control how you spend that time.

And because you own the business, not just a role in it, you’re also building wealth differently than saving a paycheck. A profitable business is an asset you can grow, sell, or pass down. Business ownership builds long-term value in a way that employment typically doesn’t.

The real advantage, though, goes beyond money. Impact and innovation give your work meaning beyond the paycheck. You solve a real problem for real people. Every customer who benefits from your product is someone whose life got a little easier because of something you built.

Career independence also opens the door to multiple income sources as your business matures. Many entrepreneurs combine their main venture with other approaches, such as freelancing, consulting, or passive income, all proven ways to make money without a traditional job.

What are some of the common mistakes new entrepreneurs make?

Most entrepreneurial mistakes follow the same pattern: spending too much time, money, or energy in the wrong place at the wrong time. Here are the five that keep coming up:

- Overplanning without action. Writing a 40-page business plan feels productive, but it’s not the same as testing an idea in the market. Plans don’t survive first contact with real customers. Ship something small, get feedback, and adjust. That’s the plan.

- Skipping idea testing. Building a full product without confirming demand can waste months of effort and significant money. Talk to potential customers before building anything. If possible, try to pre-sell your product or offer a pilot service to confirm people are willing to pay. Many startup failures happen because founders skip or rush this step.

- Ignoring the numbers. Some entrepreneurs track revenue but overlook expenses, while others avoid financial tracking altogether. You need to know how much it costs to acquire a customer, your profit margins, and how much you spend each month. Without clear financial visibility, businesses can run out of cash before the founder realizes there’s a problem.

- Scaling too fast. Adding more customers before your product and processes are stable is like pouring water into a leaking bucket. More customers will simply create more complaints and operational stress. Before expanding, focus on improving product quality, fixing operational gaps, and retaining your existing customers.

- Working without feedback. If you’re not regularly talking to customers, reading reviews, and observing how people use your product, you’re making decisions based on assumptions. Build a regular feedback loop into your routine by speaking with customers, reviewing feedback, and tracking how people interact with your product or service.

All five mistakes share the same root cause: acting on assumptions instead of real evidence. Test ideas early, monitor your numbers, listen to customer feedback, and adjust your approach before small issues turn into costly problems. And as your business grows, make sure your marketing strategy evolves as well, whether you’re selling through your own website, social media channels, or marketplaces like Amazon and Flipkart. Even the best product won’t sell itself without the right visibility.

How to launch your business online with the right tools

Many modern entrepreneurs launch their business online first because it cuts costs, speeds up testing, and puts their offer in front of a global audience from day one. You don’t need a physical storefront to start earning revenue.

A website isn’t just a marketing tool; it’s a business asset. It builds credibility with customers who search for you, drives traffic from search engines, and gives you a direct sales channel without relying on third-party platforms that take a cut.

Here’s the five-step process to get your business online:

- Choose your business model – service, ecommerce, digital product, or SaaS. This decision shapes everything from your site structure to your payment setup.

- Pick a domain name that reflects your brand. Keep it short, memorable, and easy to spell.

- Build a professional website to showcase your offer. This is where customers learn about you, compare you to alternatives, and decide whether to buy. Even businesses that start on Instagram, WhatsApp, or marketplaces benefit from having a website as a central hub.

- Set up secure payment processing and analytics tracking. You need to accept money and measure what’s working from the very first visitor.

- Launch publicly and collect customer feedback for your next round of improvements.

Building your site early gives you two advantages beyond revenue. First, it helps your search rankings – the sooner your site is live, the sooner search engines start sending visitors your way. Second, it builds trust. People check your website before they buy from you. A professional online presence signals that you’re a real business, not a side project.

You don’t need coding knowledge to launch a professional site. Website builders and web hosting platforms handle the technical setup so you can focus on your business. Ecommerce features let you sell products and services directly from your site, and reliable hosting keeps your pages fast and online as your traffic grows.

Think of this as the final connection point in the whole process: you found a problem, tested a solution, built an MVP, figured out your business model – and now you’re putting all of it online where customers can find you, pay you, and come back.

The best time to start is before you feel ready. Your first version won’t be perfect, and it doesn’t need to be. Starting an online business is one of the lowest-risk ways to become an entrepreneur today – and every step here is designed to get you there faster, with fewer costly mistakes along the way.

All of the tutorial content on this website is subject to Hostinger's rigorous editorial standards and values.

Alma is an AI Content Editor with 9+ years of experience helping ideas take shape across SEO, marketing, and content. She loves working with words, structure, and strategy to make content both useful and enjoyable to read. Off the clock, she can be found gaming, drawing, or diving into her latest D&D adventure.